Sydney rental yields at new low

Sydney rents dropped over December, forcing yields down to a record low of 3 per cent, according to property researcher CoreLogic. Melbourne rents managed growth of 1.4 per cent but this did not stop yields falling to 3.3 per cent, while looking likely to hit 2017 lows of 3.1 per cent this year.

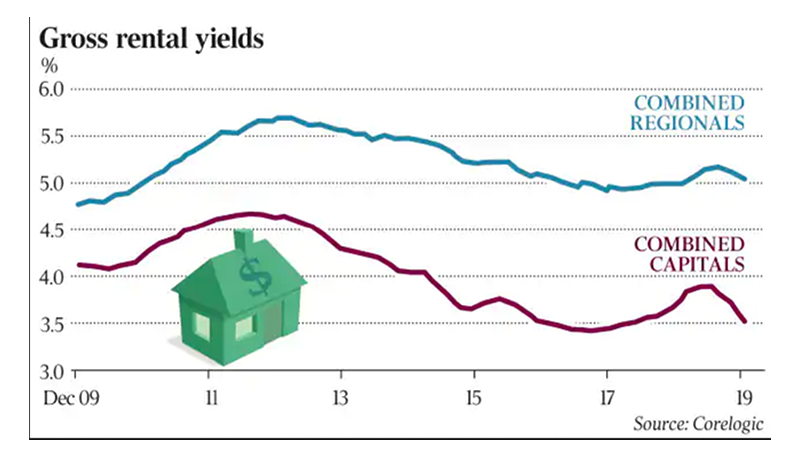

Nationally rents grew 1.2 per cent on an annualised basis, but the increase in property prices saw yields fall 0.2 per cent to 3.8 per cent through 2019.

CoreLogic’s head of research, Tim Lawless, said investors needed to be strategic going forward.

“It all depends on your investment philosophy,” he said. “Inherent scarcity and demand in blue-chip suburbs offer good capital gains but lower yield profiles.”

Financial planner William Bracey told The Australian, investors needed to moderate their expectations around returns from residential property.

He said continually growing house prices and increased supply in the marketplace had made the 5 per cent yields that were taken for granted in the 1980s and 1990s now unattainable.

“It’s not just prices going up, but there is also a lot more stock on the market,” Mr Bracey said.

“Without a shortage, people now have choices. Therefore, it’s a pressure on yields because people aren’t going to pay as high rents.”

Mr Bracey suggested alternative investment options.

“People are always chasing yield but it’s just not there, certainly not in residential,” he said. “But interestingly enough, commercial real estate is still holding up okay.

“Generally speaking, commercial property prices have held and the yields have held reasonably well. For argument’s sake, in a well diversified commercial property fund, you may be getting 5 per cent or 6 per cent yield.”

Outside of the major cities, the tight rental market of Hobart was one of the strongest in the country, with investors benefiting from relatively affordable property and strong housing demand. Rents grew 6 per cent over the year, while yields rose to 5.1 per cent.

Darwin and Perth also grew to offer returns of 5.9 per cent and 4.3 per cent respectively. Adelaide (4.4 per cent) and Brisbane (4.5 per cent) yields held through 2019.

Independent economist Andrew Wilson said that while investors had been generally sluggish to get back into the market with tight lending acting as a barrier to entry, the fertile economic environment still made residential property a sound investment.

“We have a low yield economy at the moment and I think more investors generally will be looking at property given the potential for capital growth and what remains still a tax positive environment, in terms of those tax policies including negative gearing, tax depreciation to discounts on capital gains. You would expect to see more invested in the market,” Mr Wilson said.

Still have some questions?

If you want to discuss your property portfolio or investment property with one of our planners. Call us to arrange an appointment on 02 9328 0876.

Article by Mackenzie Scott | The Australian

Copyright The Australian – First Published in the Australian 03 January 2020 – https://www.theaustralian.com.au/business/property/sydney-rental-yields-at-new-low/news-story

Mackenzie Scott is a property and general news reporter based in Brisbane. Prior to joining The Australian in 2018, she was the editorial coordinator at NewsMediaWorks, covering media and publishing, and editor at travel and lifestyle website Xplore Sydney.

General Disclaimer: This article contains information that is general in nature. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decisions based on this information. Please seek personal financial advice prior to acting on this information.