Protecting your wealth – Insurance in plain English

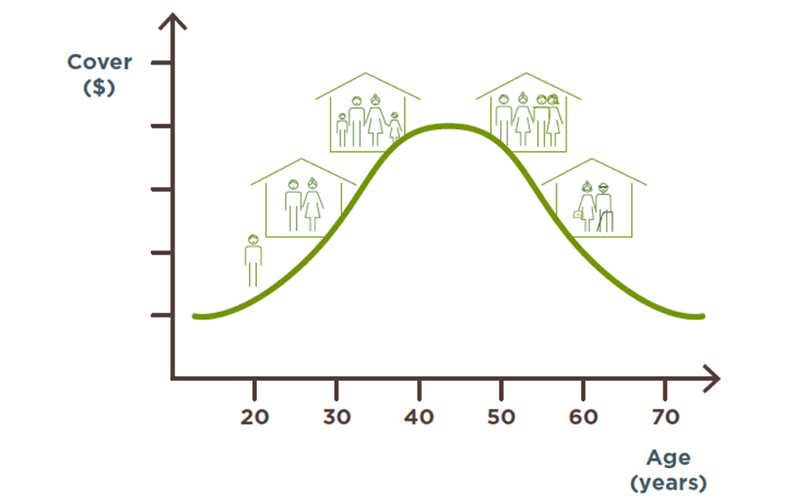

Everybody’s circumstances are different, but insurance is important for everybody. Your need for insurance will change as you move through the different stages of your life.There are many different types of insurance, and we can help you find the right level of protection for your needs.

What types of insurance are there?

There are many types of insurance.

Car or home/contents insurance allows you to insure your belongings. Personal insurance policies enable you to insure yourself and your ongoing wellbeing.

Personal insurance provides protection against sickness, injury and death, and includes:

- Life insurance

- Total and Permanent Disability (TPD) insurance

- Trauma insurance, and

- Income protection.

While insurance doesn’t remove the risk of something going wrong, it provides you and your family with protection and financial security if something does happen.

The amount of insurance you need is affected by:

- how much you earn

- your cost of living

- your assets

- your liabilities

- your relationship status (whether you are married, in a de facto relationship or single), and how many dependants you have.

Life insurance

Life insurance protects your family by paying a lump sum if you die. Most people think that life insurance is only for the main income earner, but the person who takes care of the family is also a large contributor to the home and can be insured.

| Life Insurance | |

|---|---|

| Can be purchased inside or outside of superannuation | Many super funds provide life insurance. Premiums can be paid from contributions made to your fund by your employer, by you personally or simply deducted from your account balance in the fund. |

| Tax treatment |

Outside super

Inside super

|

Total and Permanent Disability insurance

TPD cover provides a lump sum payment if you suffer a disability before retirement and can’t work again, or can’t work in your usual occupation or chosen field of employment.

| Total and Permanent Disability insurance | |

|---|---|

| Can be purchased as an add on, or as a stand alone | You can buy TPD as an add on to term life insurance, or as a stand alone product. You can also get TPD as an extra benefit from your super fund or as part of a trauma insurance product. |

| Tax treatment |

Outside super

Inside super

|

Trauma insurance

Trauma (or critical illness) insurance provides a cash lump sum if you suffer a specified illness or injury. Advances in medical treatment have increased the need for trauma insurance. The improved chance of survival means that although you are more likely to survive, you are also more likely to have substantial medical bills to pay.

| Trauma Insurance | |

|---|---|

| Stand alone policy or additional options | Trauma insurance is usually purchased as a stand alone policy, but can be purchased with additional options, such as a TPD benefit. Trauma insurance is generally not available through superannuation. |

| Cost | Trauma cover is relatively more expensive than other forms of life insurance because of the greater probability of a trauma event occurring. |

| Tax treatment |

|

Income protection

Income protection insurance (also known as salary continuance or income replacement) provides a monthly payment to replace lost income if you are unable to work due to injury or sickness.

| Income protection | |

|---|---|

| Level of cover | The maximum allowable cover is generally 75 per cent of your gross wage. |

| Benefit period | The longer the benefit period, the higher the premium. |

| Can be purchased inside or outside of superannuation | Income protection is available through your super fund or can be purchased as a stand alone policy outside of super. |

| Tax treatment |

|

Insurance as part of your superannuation

Life, TPD and income protection insurances are all offered within superannuation. If your insurance is held within superannuation, the cost of the premiums is withdrawn from your superannuation balance.

It is important to work out the best way to structure your insurance, whether inside or outside superannuation, or a combination of the two.

Benefits to having insurance in your superannuation may include:

- automatic acceptance – there’s generally no need to complete medical checks

- cheaper cover – from the bulk discount typically available to superannuation funds, and

- tax deductibility – some contributions to superannuation attract a tax deduction, so you may be able to pay your premiums by making tax deductible super contributions.

Disadvantages of having insurance in your superannuation include:

- limitations on the types of cover available

- potential delays in the payment of benefits in the event of death, and

- high tax rates – superannuation death benefits paid to a non-dependant may be taxed at up to 32 per cent.

Keep your insurance up to date

Insurance is not static, and your need for cover will change as you move through different stages in your life. As part of the financial advice process, we regularly review your insurances to make sure that you are adequately protected if your circumstances change.

Are your insurances up to date?

Or do you need to put something in place to better protect youself? To arrange an appointment to speak with one of our advisors call us on 02 9328 0876.

This article contains information that is general in nature. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decisions based on this information.