The new measures include initiatives for individuals, households and businesses. Business initiatives include measures to both enhance cashflow and provide easier access to credit.

Enabling legislation (where required) is expected to be introduced to Parliament in the sitting week commencing 23 March 2020.

The proposed measures are briefly summarised below and will require passage of legislation and/or regulations to provide certainty as to the specifics of the proposals.

Federal Budget: the Government has also announced that due to continuing uncertainty associated with the Coronavirus pandemic that the Federal Budget which was due to be handed down in May will be deferred until 6 October 2020.

1. Measures to support individuals & households

Proposed effective date: various, see below.

Temporary early access to superannuation.

Proposed effective date: 2019-20 and first quarter (approx.) 2020-21. Applications available from mid-April 2020.

The Government recognises that immediate financial necessities may temporarily outweigh the stated purpose of superannuation as a retirement savings vehicle and will temporarily allow additional early access to super savings in prescribed circumstances.

People who meet the below criteria will be allowed to access:

- up to $10,000 of their super before 1 July 2020, and

- up to an additional $10,000 in the three months starting from 1 July 2020 (timeframe is approximate and subject to legislation).

Amounts released under these rules will be paid tax-free and will not affect Centrelink or DVA payments.

Individuals eligible to apply for early release include:

- Those who are unemployed; or

- Those eligible to receive Jobseeker Payment, equivalent Youth Allowance, Parenting Payment, Special Benefit or Farm Household Allowance; or

Those who on or after 1 January 2020:

- Were made redundant; or

- Had their working hours reduced by 20% or more; or

- As a sole trader, their business was suspended or turnover decreased by at least 20%.

Those eligible must apply to the ATO through the MyGov website and must self-certify that they meet the above requirements. The ATO will then process the application and issue a Determination to the applicant and their super fund.

The super fund will be able to then pay the applicant directly. Those eligible will only be allowed one withdrawal application in each period (i.e. cannot ‘top-up’ by making a second request if an original withdrawal for less than $10,000 was made).

Applications for early release of super under this measure are expected to commence from mid-April 2020, approval and benefit payment time frames have not been announced at the time of writing.

Early release of super benefits under this measure will also be available to members of SMSFs.

Accessing super benefits in times of market down-turns is usually not recommended as it may crystallise losses. However members who experience loss of employment or a significant decrease in income may find this measure provides immediate financial relief and the basis to re-build.

Further details of this measure are available in this fact sheet released by Treasury.

Support for retirees – temporary reduction in minimum pension drawdown requirements

Proposed effective date: Financial years 2019-20 and 2020-21.

Similar to measures that applied following the 2008 Global Financial Crisis, the Government has proposed a 50% reduction in the minimum income drawings required from account based pensions and similar products for the 2019-20 and 2020-21 income years.

This measure is designed to allow those whose circumstances permit to reduce income payments from their superannuation based pensions or income streams so as to minimise the need to sell down assets in depressed markets.

Those who have already taken 50% or more of the required minimum payment in the 2019-20 financial year could contact their fund and cease any further payments until 30 June (subject to passage of regulations/legislation).

This measure is not compulsory. Individuals who need the income or simply do not wish to reduce their income payments need not take action.

Superannuation pensioners who are funding their income requirements from a cash account may also decide to take no action.

Details of this measure are available in this Fact Sheet released by Treasury.

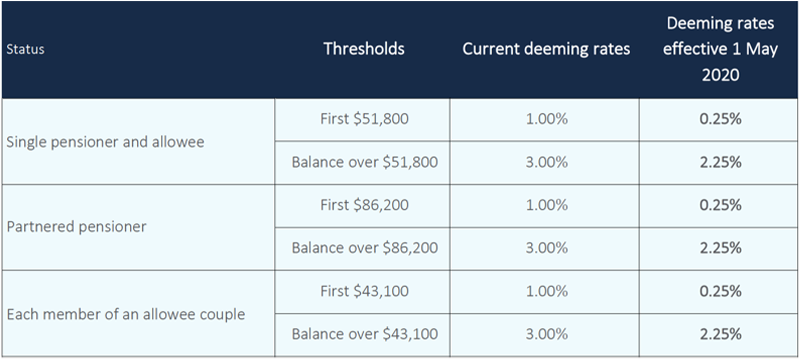

Support for retirees and income support recipients – further reduction in deeming rates

Proposed effective date: 1 May 2020.

Adding to the 12 March 2020 announcement, the Government has announced a further 0.25% reduction in deeming rates.

This will mean that part-rate pensioners and allowees will have less income assessed from their financial investments. If a recipient is income tested, the effect of the reduced deeming rate may result in an increase in social security entitlements.

Any increase in the amount of income support received due to the reduction in deeming rates will commence to flow through to clients’ bank accounts from 1 May 2020.

The following table illustrates the new deeming rates:

Table 1: Reduction in deeming rates

Payments to income support recipients (households)

Proposed effective date: various, see below.

The Government will now provide two payments of $750 to eligible social security, veteran and other income support recipients (including concession card holders). Each $750 payment is a set amount, regardless that the recipient may have multiple eligibility (e.g. be an income support recipient and concession card holder).

The first payment will be made to those receiving eligible income support or other benefits as at 12 March 2020, or those who have applied for a benefit as at that date (or up to 13 April 2020) and are subsequently approved.

The second payment will be available to those who are eligible income support recipients or concession card holders as at 10 July 2020 and will be paid automatically from 13 July 2020. However, those who are receiving a payment that is eligible to receive the Coronavirus supplement (see below) will not receive this second $750 payment.

Each eligible person in a household can receive the payment (e.g. a pensioner couple would receive a total of $1,500 in each round of payments).

The payments will be exempt from tax and not included in the income test for social security, veteran or Farm Household Allowance payments.

Eligible recipients must be residing in Australia. For the first payment, eligible benefits include:

- Age Pension

- Disability Support Pension

- Pension Concession Card

- Carer Payment and Allowance

- Commonwealth Seniors Health Card

- Veteran and War Widow(er) payments

- Veteran Gold Card

- Youth Allowance

- Newstart Allowance/Jobseeker payment

- Farm Household Allowance

- Family Tax Benefit

- Parenting Payment

- Austudy

- Partner Allowance

The first payment will be made from 31 March 2020 with 90% of payments expected to be made by mid-April 2020.

The payment will be made automatically to income support recipients. Those whose only qualifying benefit is a concession card will be contacted to confirm bank account details.

In addition, eligibility criteria for benefits such as Sickness Allowance and Youth Allowance or other study related payments will be relaxed where the recipient can demonstrate inability to work or lack of compliance is due to Coronavirus related causes.

To be eligible for the second payment the person must be residing in Australia and receiving one of the payments or concession cards listed above except for payments which receive the Coronavirus supplement (see below).

These excluded payments include: Jobseeker Payment, equivalent Youth Allowance, Parenting Payment, Special Benefit or Farm Household Allowance.

The Government Fact Sheet on Payments to Households is available from Treasury.

Enhanced income support for individuals

Proposed effective date: 27 April 2020

The Government is temporarily expanding eligibility to income support payments and establishing a new temporary ‘Coronavirus supplement’. The supplement will be paid at the fixed rate of $550 per fortnight for six months commencing 27 April 2020 and is in addition to existing income support payments.

Those eligible for the supplement include existing and new recipients of the following payments:

- The Jobseeker Payment (previously Newstart Allowance and other payments transitioning to the Jobseeker Payment);

- Youth Allowance (YA) Jobseeker Payment;

- Parenting Payment (partnered and single);

- Farm Household Allowance; and

- Special Benefit recipients.

For the period of the Coronavirus supplement there will also be expanded access to the payments listed above.

The Jobseeker payment (and YA Jobseeker payment) will be available to permanent employees who lose their jobs. These payments will also be available to sole traders, self-employed and contract or casual workers whose reduced income meets the income test criteria.

Asset testing of Jobseeker payment, YA Jobseeker payment and Parenting Payment will be waived for the period of the supplement.

The one week ordinary waiting period has already been waived and the Liquid Assets Waiting Period (LAWP) will also be waived for those eligible for the supplement. Those already serving a LAWP will have the remainder waived.

Income maintenance periods and compensation preclusion periods will continue to apply. Claimants for the Jobseeker payment will have to certify that they are not receiving or eligible for paid employer leave or accessing income protection payments.

At this time measures are also being taken to streamline the application process including reduced documentation requirements and relaxation of mutual obligation and study requirements where these are impacted by the Coronavirus.

Details of this measure are available in this Fact Sheet released by Treasury.

2. Measures to support small and medium size employers

Proposed effective date: Various – see below

With reference to the tax-free payment announced by the Government on 12 March 2020 to boost cash flow for small and medium size businesses.

The Government has now indicated it will enhance that previously announced tax-free cash flow boosting payment. Instead of the previously announced $25,000 maximum, the government is to now provide up to $100,000 (minimum payment of $20,000) to eligible small and medium-sized businesses. Payments will now also be made to eligible not for-profits (NFPs including charities) that employ people.

Small and medium-sized business entities (including NFPs/charities) with aggregated annual turnover under $50 million and that employ workers are eligible.

The payments will only be available to active eligible employers established prior to 12 March 2020. However, charities which are registered with the Australian Charities and Not-for-profits Commission will be eligible regardless of when they were registered, subject to meeting other eligibility requirements. This recognises that new charities may be established in response to the Coronavirus pandemic.

Under the enhanced arrangements, tax-free payments will be made in two stages.

First stage

Eligible businesses that withhold tax to the ATO on their employees’ salary and wages will under the first stage receive a payment equal to 100% (up from 50%) of the amount withheld, up to a maximum payment of $50,000.

Eligible businesses that pay salary and wages will receive a minimum payment of $10,000 (up from $2,000) even if they are not required to withhold tax.

The tax-free payment in this first stage will be delivered by the ATO as a credit in the activity statement system from 28 April 2020 upon businesses lodging eligible upcoming activity statements.

Second stage

In the second stage, additional payments will be made in the July – October 2020 period. To qualify for the additional second stage payments, the entity must continue to be active.

Eligible entities will receive the additional payments equal to the total of all of the boosting cash flow for employers payment they received under the first stage. This means that eligible entities will receive at least $20,000 (2 x $10,000) minimum, up to a total of $100,000 (2 x $50,000) maximum combined under both payments.

For monthly activity statement lodgers, the additional second stage payments will be delivered as an automatic credit in the activity statement system. This will be equal to a quarter of their total first stage Boosting Cash Flow for Employers payment and received following the lodgement of their June 2020, July 2020, August 2020 and September 2020 activity statements (up to a total of $50,000).

For quarterly activity statement lodgers, the additional second stage payments will also be delivered as an automatic credit in the activity statement system. This will be equal to half of their total first stage Boosting Cash Flow for Employers payment and received following the lodgement of their June 2020 and September 2020 activity statements (up to a total of $50,000).

Further details of this measure are available in this Fact Sheet released by Treasury.

Other measures announced to support the cash flow needs of small and medium-sized business entities include:

Under a ‘Coronavirus SME Guarantee Scheme’, the government will provide a guarantee of 50% to SME lenders to support new short-term unsecured loans to SMEs. The Scheme will guarantee up to $40 billion of new lending. According to the government, this will provide businesses with funding to meet cash flow needs by further enhancing lenders’ willingness and ability to provide credit.

The government is also cutting red tape by providing a temporary exemption from responsible lending obligations for lenders providing credit to existing small business customers. This reform is aimed at helping small businesses get access to credit quickly and efficiently.

As always I want to reiterate that myself and the team at SFP are here to answer ANY questions you may have during this time. Stay safe in these uncertain times, we’re in this together.

Bill and the team at SFP.

If you have ANY questions during this unprecedented time…

Please get in touch to speak with your Financial Planner we’re here to help, either book a virtual meeting of get in contact with us on 02 9328 0876.

Bill Bracey – Principal & Senior Financial Planner | Sydney Financial Planning

General Disclaimer: This article contains information that is general in nature. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decisions based on this information. Please seek personal financial advice prior to acting on this information.