Wages growth is likely to pick up to 3% this year.

A Russian invasion of Ukraine risks a short term hit to shares followed by recovery over the next 3 to 12 mths.

Introduction

This note covers the main questions investors commonly have regarding the investment outlook in a simple Q&A format.

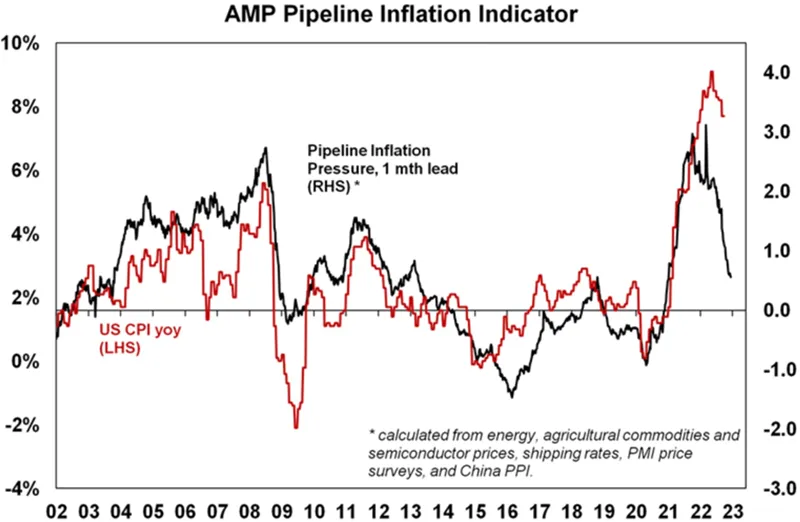

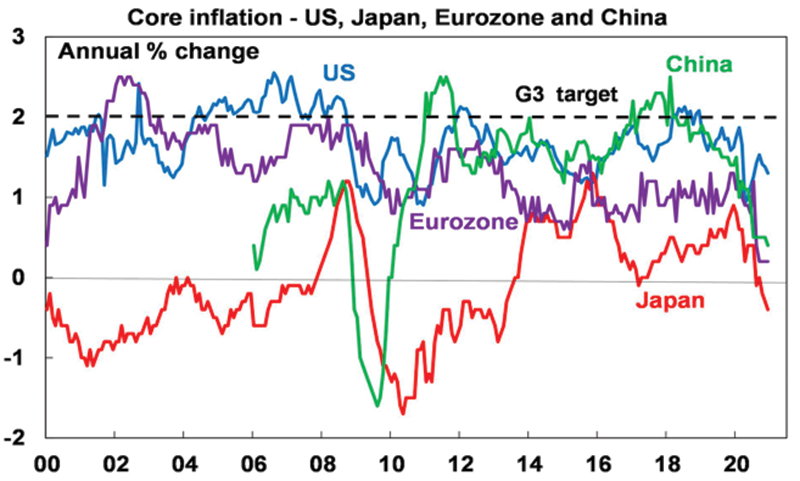

Is the rise in inflation temporary or permanent?

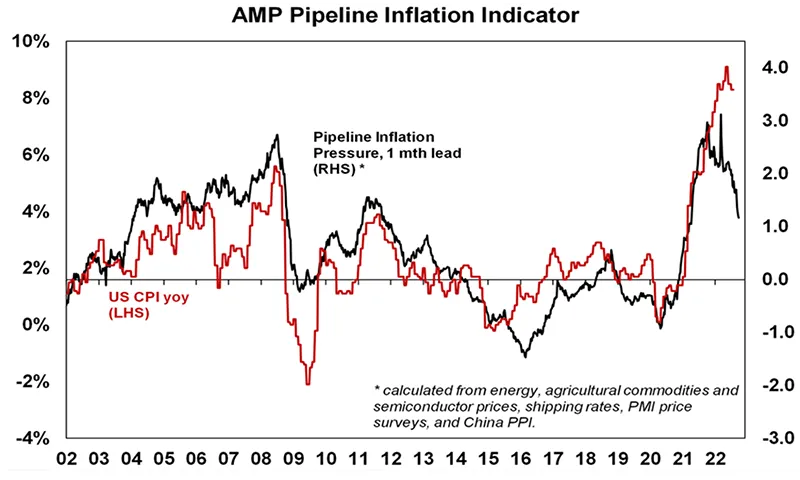

I suspect it’s a bit of both. Much of the rise in inflation (to a 40 year high in the US and to 3.5%yoy in Australia) can be traced to distortions caused by the pandemic which boosted goods demand and restricted supply (both of goods & workers). Global energy prices are also being boosted by geopolitical tensions (notably in Europe). As consumer demand rebalances back to services, workers return and production catches up to demand, inflation should subside over the next 12 months or so.

However, underlying inflation is unlikely to fall back to pre-pandemic lows and risks running above central banks targets over the next 5-10 years: we are now seeing much easier monetary and fiscal policy & many of the structural forces that drove low inflation look to be going in reverse: globalisation is in retreat; the ratio of workers to consumers is in decline; and we are now seeing bigger more interventionist government.

Will wages growth rise too?

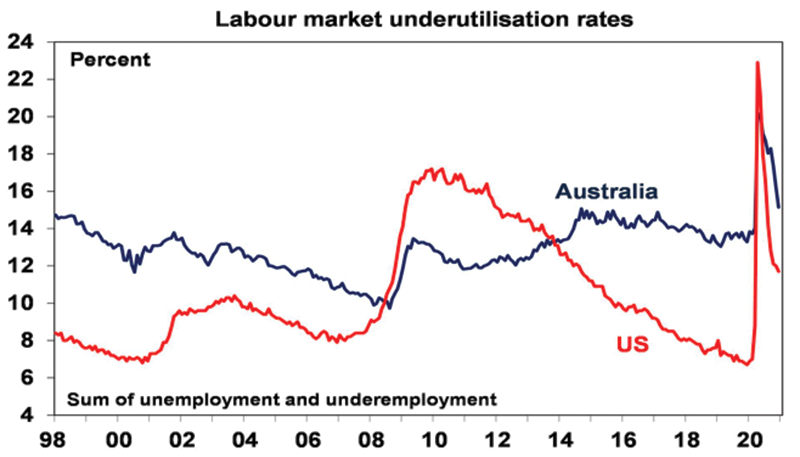

Wages growth has already lifted to 4-5% yoy in the US, depending on the measure. But it has higher inflation and has seen less workers return through the reopening than in Australia. Nevertheless, numerous signs point to faster wages growth in Australia: the jobs market is tight, pushing towards full employment; various business surveys point to rising labour costs; ABS data shows payroll wages accelerating relative to jobs; and there are numerous anecdotes of wage pressure. We expect wages growth to rise to a 3% annual pace by mid-year.

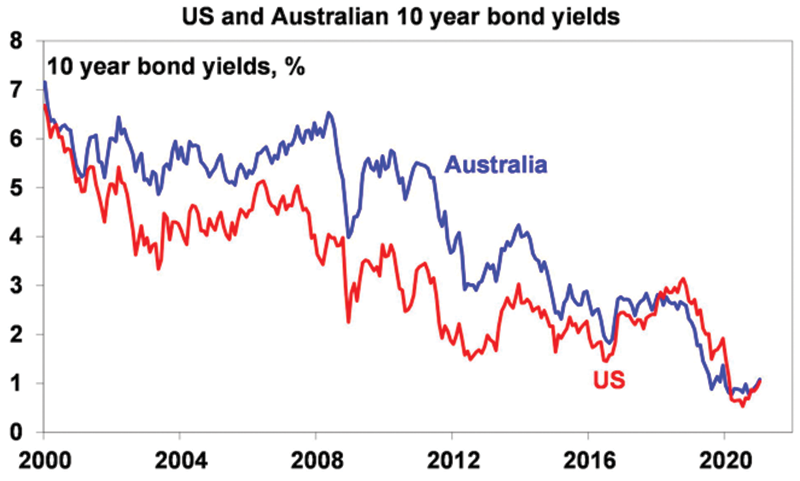

How high will Australian interest rates rise?

We expect the RBA to start raising the cash rate in August (possibly June) after news of more strong inflation data, unemployment below 4% and wages growth pushing up to 3% and see the cash rate rising to around 1.5 to 2% over the next two years or so. This would add a similar amount to variable mortgage rates. It will take household debt interest payments relative to income back to around 2018 levels. Higher household debt to income levels relative to the past and compared to say, the US, along with falling house prices will allow the RBA to proceed cautiously in raising rates through next year and see rates peak at lower levels compared to the past. Australia also has half the US’s inflation rate.

Will the end of QE & rate hikes be a double whammy?

Not really. Bond buying by central banks (or Quantitative Easing) was an alternative to cutting rates when rates had hit zero. With economic activity recovering and inflation up, it makes sense to end it and begin the withdrawal of the liquidity that was pumped in via QE (ie start quantitative tightening). But central banks can manage this with rate hikes to make sure the overall tightening in monetary conditions is not excessive.

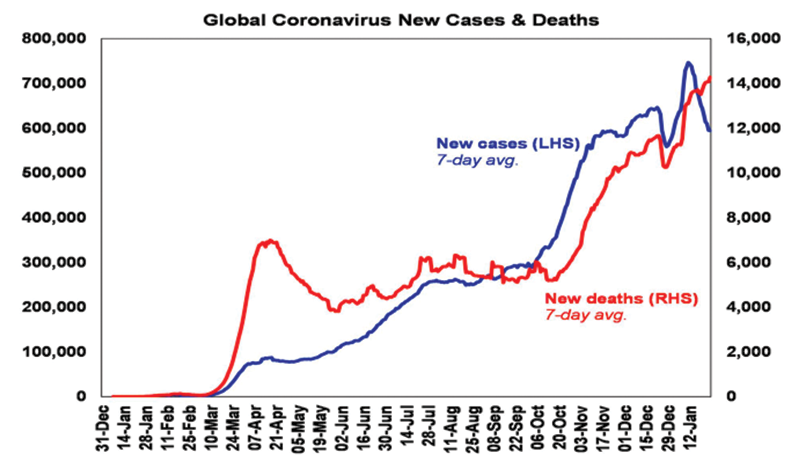

Is coronavirus no longer an economic concern?

Not quite, but nearly. Starting last year each successive covid wave seems to have had progressively less economic impact. This reflects a combination of vaccines, new treatments and recent covid variants being less harmful which has combined to enable reopening to continue. While the risk remains of a new variant which is more harmful, causing a setback, coronavirus could finally be moving from a pandemic to being endemic.

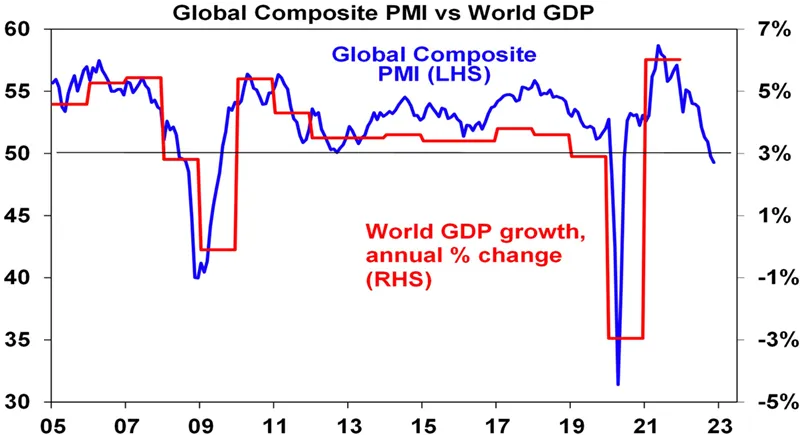

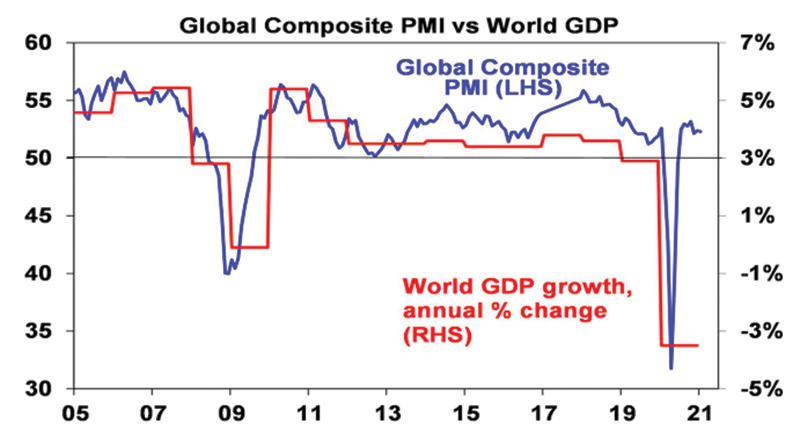

Is the economic recovery on track?

While supply side constraints, monetary tightening, geopolitical threats and covid will constrain global and Australian economic growth, it will still be reasonable at around 4.5% this year. Key drivers are likely to be: ongoing reopening; pent up demand and excess savings; still easy monetary policy; strong business investment; and low inventory levels.

How would a Russian invasion of Ukraine impact investment markets?

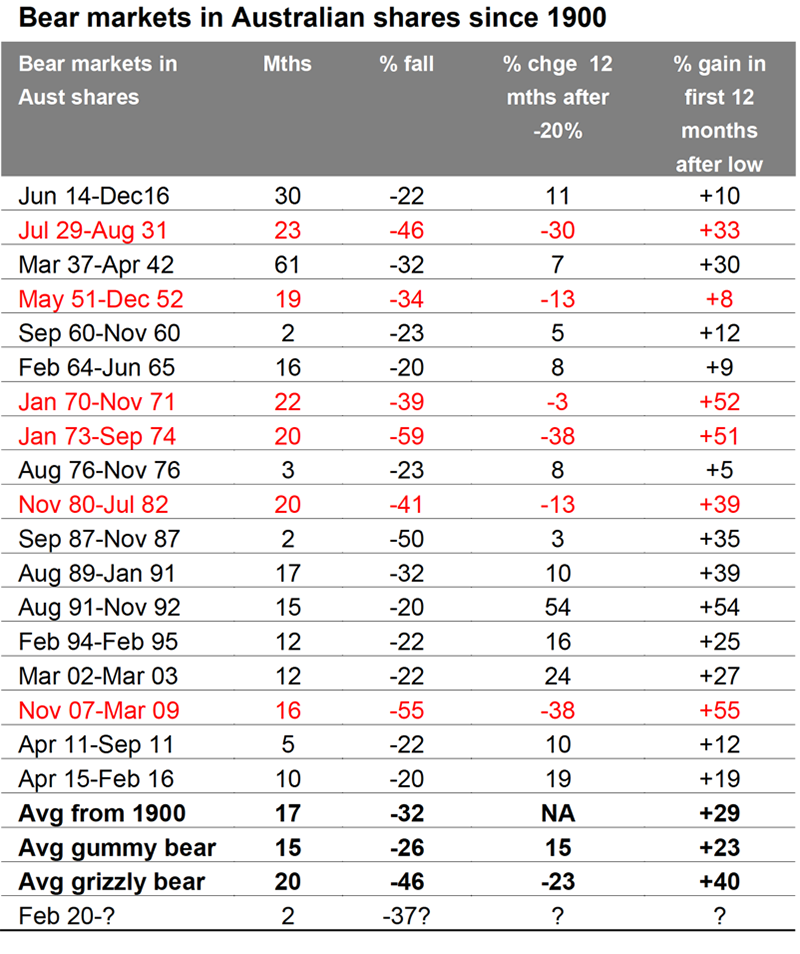

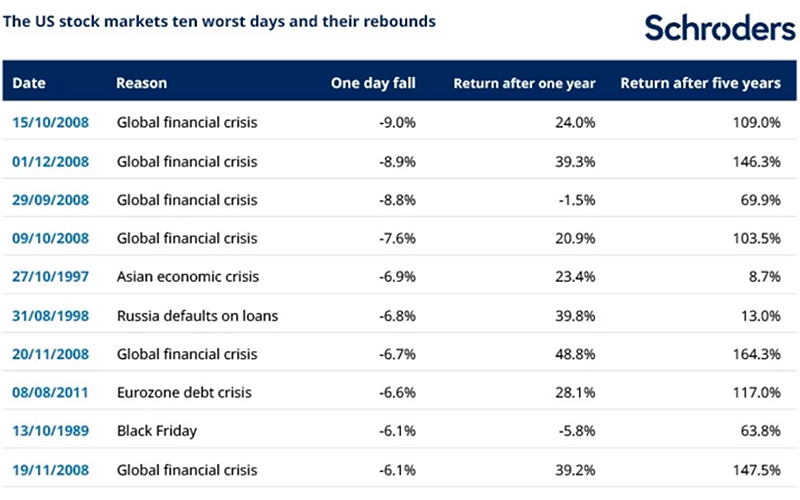

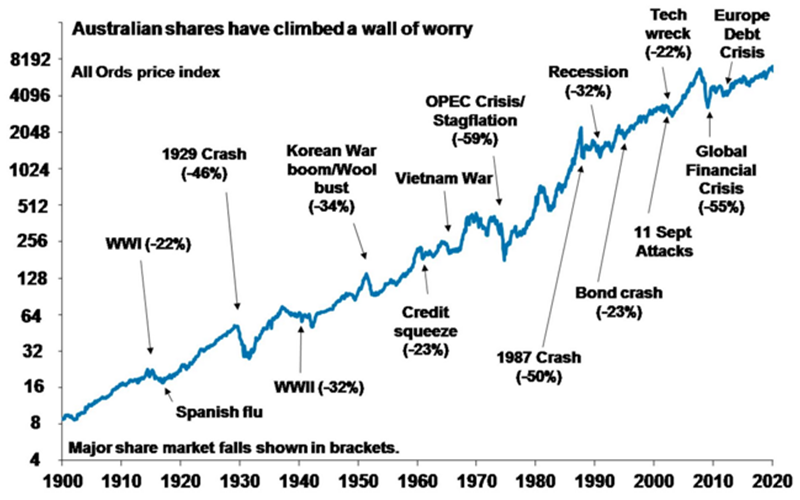

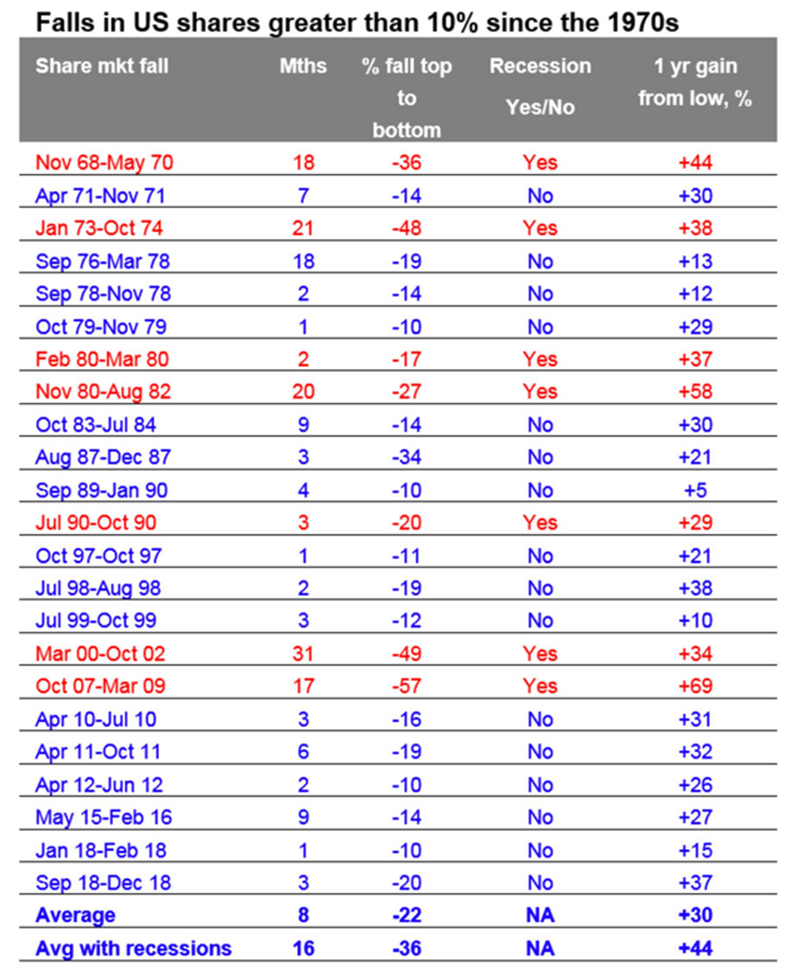

Russia has been building up its military presence on the Ukraine border and is demanding that Ukraine never join NATO and NATO not station strategic weapons there. Negotiations have made little progress as the US fears consequences in other parts of the world if NATO does not stand tough. If anything, tensions have worsened as NATO has been shoring up Ukrainian defences and Russia has built up more military assets around it, with the US warning of possible imminent invasion. However, Russia has signalled it will continue with talks. Of course, there is a long history of various crisis events impacting share markets (major events in wars, terrorist attacks, financial crisis, etc) and the pattern is the same – an initial sharp fall followed by a rebound. Based on multiple crisis since 1907 Ned Davis Research found an average decline of 7% in the US share market from such events, but 6 months later the market is up 10% on average and 1 year later its up around 15%. Put very simply, there are four scenarios:

- Russia stands down – this would provide a very brief boost for share markets, including Australian shares (eg +1%).

- Russia moves in to occupy the Donbas (which is already controlled by Russian separatists) with sanctions from the west but not so onerous that Russia cuts of gas to Europe – this could see a brief hit to markets (say -2-4%) like in the 2014 Ukraine crisis but it would soon be forgotten about.

- Russian invasion of all of Ukraine with significant sanctions and Russia stopping gas to Europe (causing a stagflationary shock to Europe & possibly globally as oil prices rise further) but no NATO military involvement – this could see a bigger hit to markets (say -10%) but then recovery over six months.

- Invasion of all of Ukraine with significant sanctions, gas supplies cut & NATO military involvement – this could be a large negative for markets (say -15-20%) as war in Europe, albeit on its edge, fully reverses the “peace dividend” of the 1990s. Markets may then take 6-12 months to recover.

Scenario 1 is still possible & it’s hard to see Russia undertaking a full invasion of Ukraine given the huge cost it would incur, let alone NATO troops being involved, but some combination of scenarios 2 and 3 are possible. But the history of such events points to an initial hit to shares, followed by a rebound.

What is the threat posed by global geopolitical tensions – including those with China?

Geopolitical issues have been building since the GFC and seemed to get a push along by the pandemic. The key drivers have been: a populist backlash against economically rationalist policies; the declining relative power of the US; and the polarising impact of social media. The most pressing are those with Russia (see above), China (in relation to Taiwan and trade with Australia) and Iran (in relation to its nuclear ambitions and oil supply). Although hard to time, they all make for a potentially more volatile ride in markets and possibly contribute to a less favourable return environment as they threaten higher inflation and less globalisation. It should be noted though that the economic impact of Australia’s tensions with China has been minor to date as most of the exports impacted were fungible commodities and able to find other markets. The same may apply in relation to iron ore if the adjustment occurs slowly.

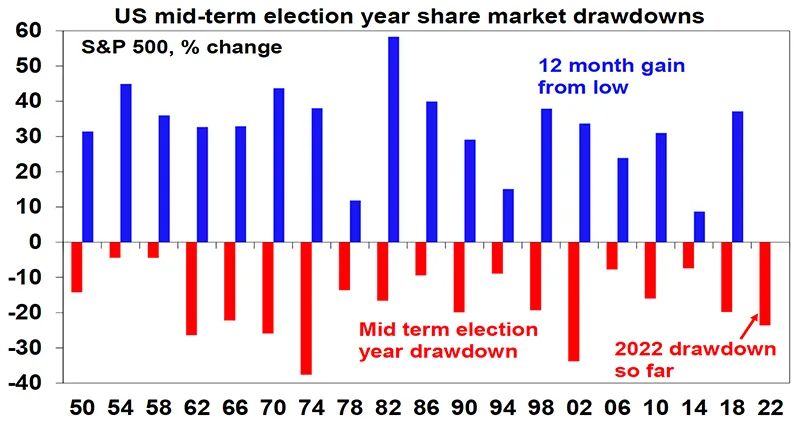

Will the Australian Federal election have much impact?

There is a tendency for Australian shares to be somewhat flat in the run up to Federal elections followed by a bounce once it’s over and this is likely to apply this year with the election likely in May. In contrast to the 2019 election where Labor offered a higher tax and higher regulation agenda the policy differences so far appear less significant and if this remains the case the impact on investment markets is likely to be minor.

What is the outlook for Australian home prices?

From their pandemic lows in 2020 Australian dwelling prices are up 25%, but the gains have been slowing since March last year. We expect a further slowing in the months ahead as a result of worsening affordability, already rising fixed mortgage rates and rising variable rates from around August with average prices peaking in the September quarter and then falling into 2024. While prices are likely to rise 3% this year, they are likely to fall -5-10% next year. Top to bottom the fall could be around -10-15%, which would take prices back to the levels of mid last year. Sydney and Melbourne are the most vulnerable to higher rates as they have worse affordability and higher debt to income levels. They are both likely to see house prices peak by mid-year and risk top to bottom price falls of around 15%, whereas other cities and regions may not peak till later this year and have more modest top to bottom price falls.

Will the return of immigrants support home prices?

The return of immigrants this year will provide some support but will unlikely be enough to stop falls given the dominant impact of higher mortgage rates in constraining demand and given the likelihood that the initial return of immigrants will be gradual and won’t offset the net negative immigration of the last two years.

How can we improve housing affordability?

This requires a multifaceted solution across all levels of government with targets to be achieved over say a five-year period. My list of policies to improve affordability includes:

- Measures to boost new supply – relaxing land use rules, releasing land faster and speeding up approval processes.

- Matching the level of immigration in a post pandemic world to the ability of the property market to supply housing.

- Encouraging greater decentralisation – the “work from home” phenomenon shows this is possible, but it should be helped along with appropriate infrastructure and of course measures to boost regional housing supply. Excess CBD office space should be speedily converted to residential.

- Tax reform to replace stamp duty with land tax (to make it easier for empty nesters to downsize & cutting the upfront burden for first home buyers) & cutting the capital gains tax discount (to end a distortion favouring speculation).

What is the outlook for commercial property?

Commercial property may see weakness in retail and office returns as the influence of the pandemic on online buying and working from home impacts as retail and office leases come up for renewal, but industrial property is likely to be strong.

Should investors invest in Bitcoin and other cryptos?

It’s hard to see Bitcoin becoming digital cash – its transactions are slow and high cost, its highly volatile and it’s a massive user of electricity. It’s not an asset generating cash flows like rent or dividends which makes it very hard to value. And it appears to move in magnified fashion relative to shares, particularly during share market falls making it a poor portfolio diversifier. All of which makes it hard to justify other than as something to speculate on! Of course, this is not to say it can’t go up further as more jump on the bandwagon. Blockchain and distributed ledger technology offer significant potential but it’s hard to separate this from the speculation around crypto currencies.

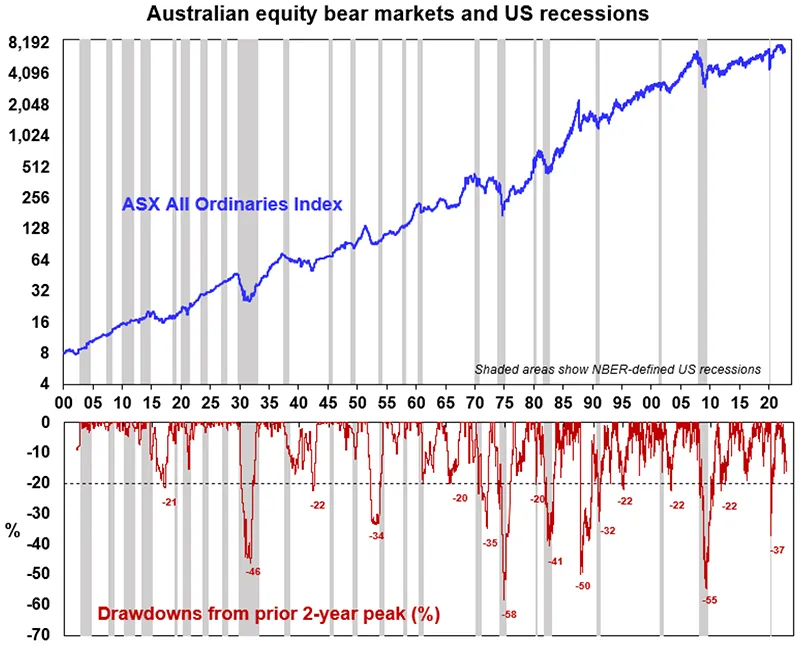

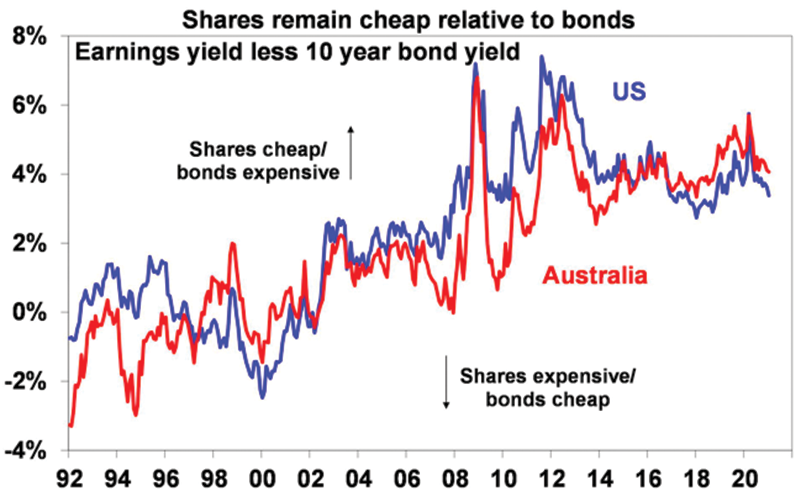

Will high inflation cause a share market crash?

Shares have had a very strong rebound from their pandemic lows and are vulnerable to higher inflation as it puts upwards pressure on interest rates and downwards pressure on share market valuations (or price to earnings multiples). However, while a crash is always a risk it’s not our base case. First, earnings expectations are still being revised up albeit not as strongly as a year ago. Second, while monetary policy will be tightened its unlikely to become so tight as to cause a recession and slump in earnings. Finally, share markets still offer a strong earnings yield premium relative to bond yields in contrast to in the year 2000 when bond yields rose above earnings yields. Of course, if inflation just continues to surge then the risks to shares will increase.

What are good hedges against higher inflation?

Sustained higher inflation will ultimately mean upwards pressure on the yield structure in the economy which is negative for investments that have benefitted from years of low and falling interest rates, like high PE tech stocks. The best protection against sustained higher inflation would be inflation linked bonds, real assets like commodities and parts of the share market that will see stronger earnings growth.

With bond yields still low why invest in bonds?

Bonds are likely to see another year of negative returns this year reflecting still low starting point yields and capital losses as yields rise. However, they are still a good portfolio diversifier as they are likely to rally if significant concerns arise about a recession.

Closing comments

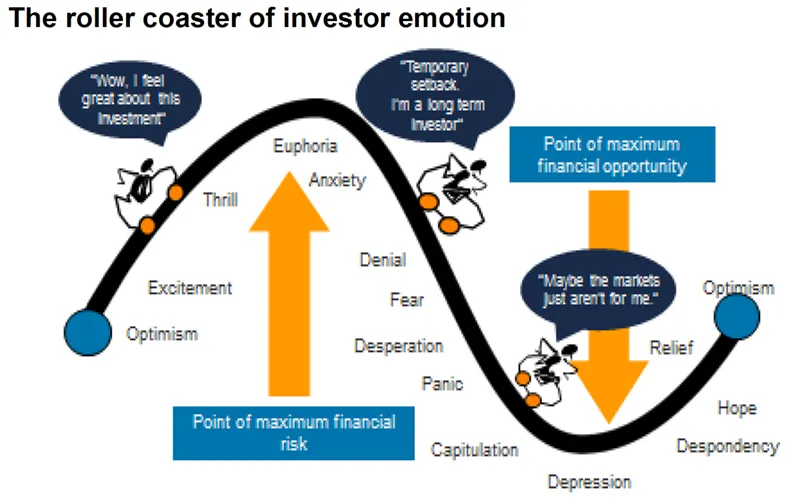

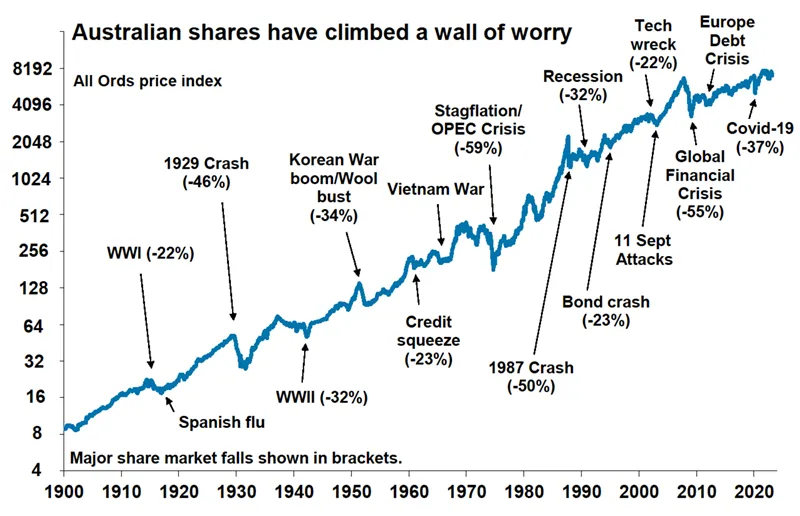

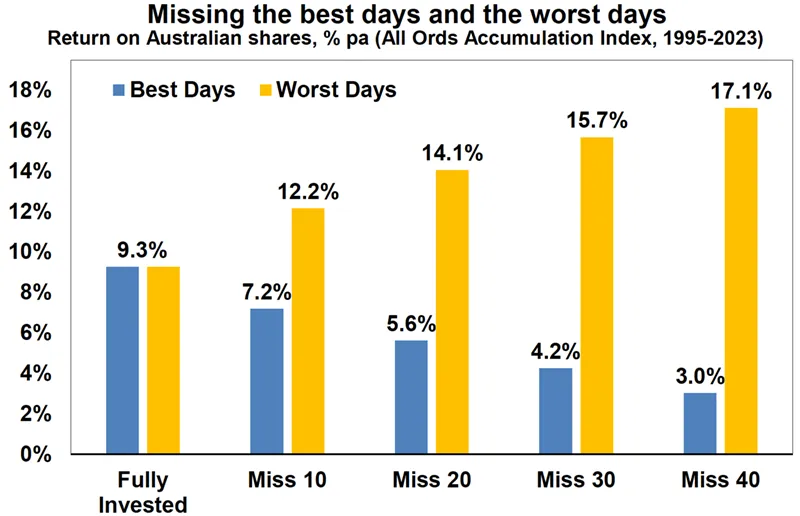

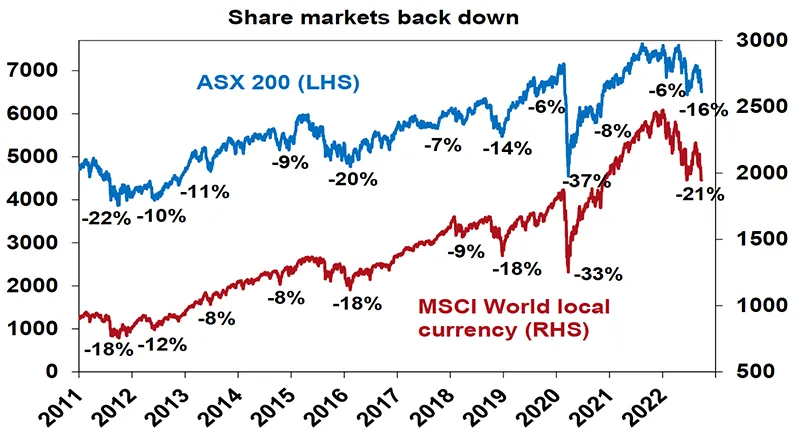

So, in closing , although we sent an economic update only 4 weeks ago, a lot has happened in the past 4 weeks and potentially a lot more can happen. It’s how we react in these times. Rather than panic, we take advantage of mispriced markets that always recover given some time.

As I also say, if you’re an advised client, you don’t need to worry. However, if you’re not regularly reviewing your investments and overall strategy with one of our Financial Planners, you need to act swiftly.

Stay calm, review if needed and ride this one out with our recommended strategies.

Bill Bracey – CEO, Managing Director

Sydney Financial Planning

Your long-term strategy and investments positioned for taking take advantage of mispriced markets?

Speak with one of our Financial Planners about the best approach for your circumstances, either book a meeting or get in contact with us on 02 9328 0876.

This article was prepared by William Bracey and Dr Shane Oliver. Dr Shane Oliver who provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets. He also provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets.

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.

General Disclaimer: This article contains information that is general in nature. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decisions based on this information. Please seek personal financial advice prior to acting on this information.